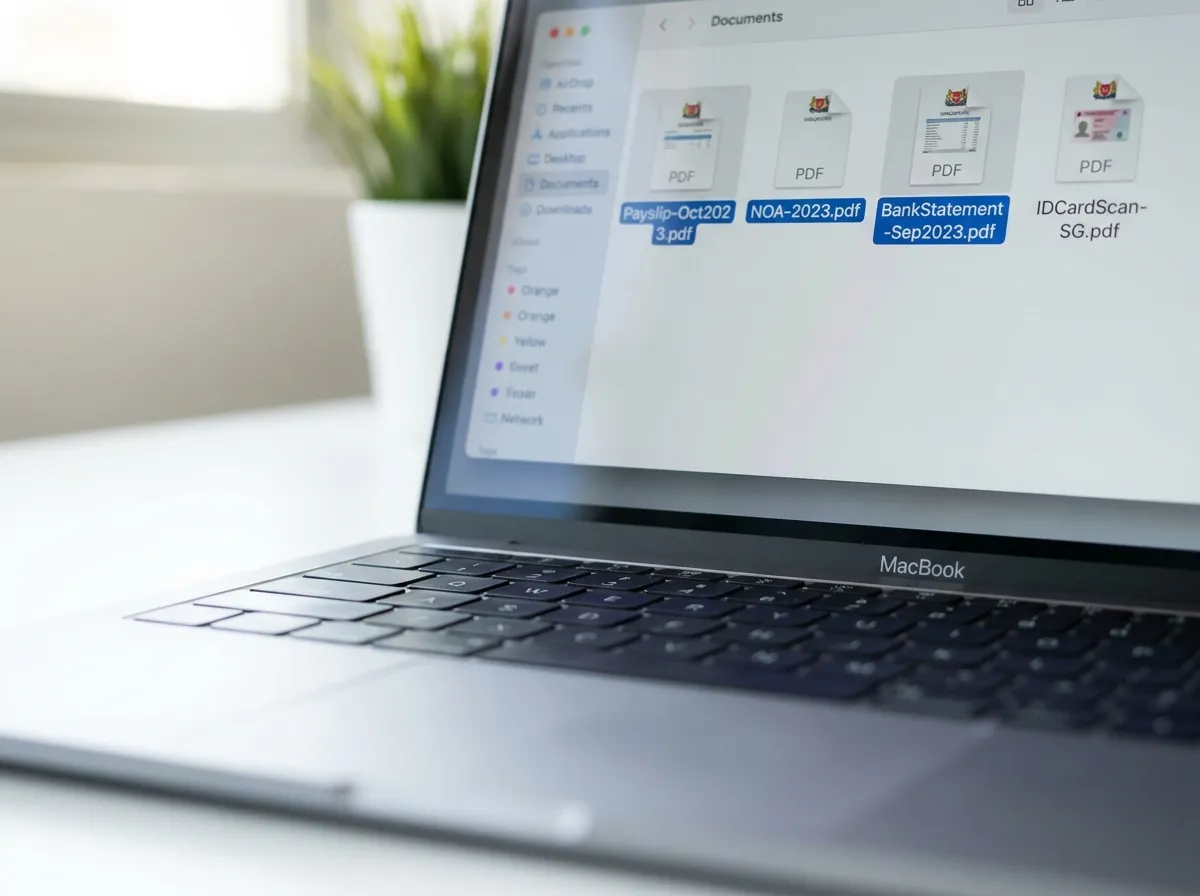

What to gather before you start.

The single biggest reason first-time applications slow down or get declined is incomplete documentation. Getting this ready before you begin removes almost all the friction.

NRIC / Passport

Proof of identity. SingPass auto-fill covers this for most applicants.

Last 3 Payslips

Proof of income for salaried employees. Most recent three months.

NOA from IRAS

Notice of Assessment from IRAS. Key income verification document.

CPF History

CPF contribution history shows stable employment and income record.

Bank Statements

Some lenders request 3–6 months of statements to verify income flow.

Self-employed?

You will also need your ACRA BizFile, NOA, and a corporate bank statement. Freelancers should add any relevant invoices or receipts as income evidence.

Explore what fits your situation better

Shorts · Lendela

Check before you consolidate

Shorts · LendelaThe numbers that actually matter.

There are three figures to understand before you compare any loan offer. Most first-timers focus on the advertised rate. Here is why that is the least useful of the three.

EIR

Effective Interest Rate

The true annual cost of borrowing. It includes how interest compounds as you repay monthly, plus any fees the headline rate leaves out. Always higher than the advertised rate. For most bank personal loans, roughly 2 to 3 times higher.

Processing Fee

One-time charge on approval

Sometimes deducted upfront from your disbursement. If you borrow $10,000 and the processing fee is 2%, you receive $9,800 in hand but repay $10,000 plus interest. Always check whether it is included in the EIR figure.

Total Payable

Principal plus interest plus all fees, across the full tenure. This is the single most comparable number across different offers. If you can only check one figure before choosing, make it this one.

How applying affects your credit file.

Each formal application you send triggers a hard enquiry on your Credit Bureau Singapore (CBS) report. As a first-time borrower, your credit file may be thin, which makes each enquiry carry more weight. Multiple applications in a short window can signal financial stress to lenders and reduce your approval chances across all of them at once.

The better approach is to apply through one channel that surfaces multiple offers from a single enquiry, rather than applying separately to each institution.

Save this · Share this

Before you apply — the first-timer's checklist

- 1

Prepare your documents

NRIC, last 3 payslips, NOA from IRAS, CPF history. Have them ready before you start.

- 2

Know the full cost

Look at EIR and total payable, not just the advertised rate. Compare on the same tenure.

- 3

Check your repayment capacity

Ensure the monthly repayment fits comfortably within your budget. Not just barely possible.

- 4

Apply through one channel

Avoid multiple applications. Each hard enquiry leaves a mark. Get matched to multiple offers from a single application instead.

- 5

Only commit when the offer fits

Accept only the offer whose monthly repayment you can sustain for the full tenure.

What the repayment commitment looks like.

A personal loan is a fixed monthly commitment for the full tenure you choose. Unlike a credit card, there is no minimum payment option. The amount is due every month regardless of what else is happening.

The key is choosing a tenure and amount that leave enough breathing room for everything else that comes up.

A useful rule of thumb

Your total monthly debt obligations, including this loan, should not exceed 40% to 55% of your gross monthly income. TDSR regulation sets 55% as the regulatory ceiling, but staying closer to 40% gives you more financial flexibility.